India is home to one of the largest middle income people in the world. They are expanding at a faster rate with each year. Similarly, Indian lending and banking industry is a rapidly evolving market which is growing at comparatively faster rates compared to other countries. Indians now can afford things like owning a house, car, credit cards etc in a much easier way compared to the earlier decades. But this easy availability to finance in form of loans and advances has created a tendency among individuals to take more than what they can really afford. LoanKuber presents some important points on how much loan or more specifically EMI one can optimally afford to repay in a peaceful manner. This is especially more applicable to loans with longer tenures like Loan against Property or Home Loans.

India is home to one of the largest middle income people in the world. They are expanding at a faster rate with each year. Similarly, Indian lending and banking industry is a rapidly evolving market which is growing at comparatively faster rates compared to other countries. Indians now can afford things like owning a house, car, credit cards etc in a much easier way compared to the earlier decades. But this easy availability to finance in form of loans and advances has created a tendency among individuals to take more than what they can really afford. LoanKuber presents some important points on how much loan or more specifically EMI one can optimally afford to repay in a peaceful manner. This is especially more applicable to loans with longer tenures like Loan against Property or Home Loans.

Income – Income is the most important input to calculate EMI in any EMI calculator for Loan against property. For  self employed businessmen or professionals this can be calculated by taking their net profit after deducting all expenses and obligations. For salaried individuals, their gross salary would be taken into account for calculating EMI. The EMI can easily be calculated through online EMI calculators.

self employed businessmen or professionals this can be calculated by taking their net profit after deducting all expenses and obligations. For salaried individuals, their gross salary would be taken into account for calculating EMI. The EMI can easily be calculated through online EMI calculators.

Expenses – EMI calculations with EMI calculators should also include expenses that you currently have, like your travelling expenses, regular expenses, obligations etc. If someone is looking for a longer tenure loan like Loan against Property, then expenses like children’s education, medical exigency, etc can also be considered. High inflation would also increase your expenses in future.

FOIR – Most banks calculate eligibility on their EMI calculators for Loan against Property with FOIR. FOIR stands for Fixed Obligations to Income Ratio. While calculating FOIR, Banks take into account all your fixed obligations like monthly EMI on term loan, Loan against Property etc. Statutory deductions like provident fund, professional tax and deduction for investments like fixed deposits are not taken into account while calculating FOIR.

FOIR – Most banks calculate eligibility on their EMI calculators for Loan against Property with FOIR. FOIR stands for Fixed Obligations to Income Ratio. While calculating FOIR, Banks take into account all your fixed obligations like monthly EMI on term loan, Loan against Property etc. Statutory deductions like provident fund, professional tax and deduction for investments like fixed deposits are not taken into account while calculating FOIR.

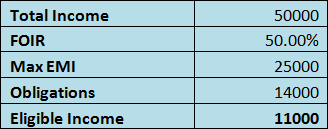

All banks and lending institutions have fixed criteria regarding FOIR. Usually, FOIR of 30% to 50% is offered to applicant of Loan against Property. This percentage is not fixed and can increase or decrease depending on income of the applicant. If you are a having higher income, higher FOIR can be offered to you. Let us look at a simple example on how to calculate FOIR-

Let us suppose you apply for Loan against property in a Bank. Your monthly income is Rs. 50,000 and you are  currently having a Car loan and a Personal loan from different Banks. Car loan has a monthly EMI of Rs. 10,000 and for Personal Loan you pay Rs. 4000 per month. The bank may have a standard of 50 percent of FOIR. So, the total installments that you can pay, as per the bank’s FOIR standard is Rs 25,000 per month. As you are already paying Rs. 14,000 per month, so your total eligibility per month would be Rs. 11, 000 for Loan against Property on bank’s EMI calculator.

currently having a Car loan and a Personal loan from different Banks. Car loan has a monthly EMI of Rs. 10,000 and for Personal Loan you pay Rs. 4000 per month. The bank may have a standard of 50 percent of FOIR. So, the total installments that you can pay, as per the bank’s FOIR standard is Rs 25,000 per month. As you are already paying Rs. 14,000 per month, so your total eligibility per month would be Rs. 11, 000 for Loan against Property on bank’s EMI calculator.

To increase your final disbursed amount, you can ask for longer tenure loan or loan at lower interest rate.

To increase your final disbursed amount, you can ask for longer tenure loan or loan at lower interest rate.

Lifestyle – Lifestyle along with personality is also an important factor while calculating your affordability for an EMI. EMI for longer term loans like Loan against Property can go for 5 to 10 years. During this time you may have to cut your outside expenses like outside food, movies and travel. To get rid of EMI burden soon, you can ask for a shorter loan duration.

Credit cards – There is a tendency among people to pay their EMIs from their credit cards. This is not a good practice as it creates another obligation to pay off your existing obligation. Also a default on credit card payment would reflect very badly on your CIBIL  record too.

record too.

Everyone wants an easy access to financing and loans. But, as we have discussed in this article it is very important to assess how much EMI you can pay for Loan against Property by analyzing your income, expenses, FOIR, personality and lifestyle etc. By calculating your optimal EMI you can save yourself from a bad CIBIL due to EMI default. A bad CIBIL would decrease your future chances of getting a loan.

We at LoanKuber can assist you in determining your optimal EMI for Loan against Property and fulfilling your dream of getting a Loan against Property for longer tenures. Also, you can use our online EMI calculator on https://loankuber.com/